Residential Status in India

Determination of residential status for taxation purpose in India

For the purpose of income tax in India, the income tax laws in India classifies taxable persons as:

- A resident

- A resident not ordinarily resident (RNOR)

- A non-resident (NR)

Each category has different tax implications. This guide will help you understand how residential status is determined and its impact on your tax obligations.

Resident

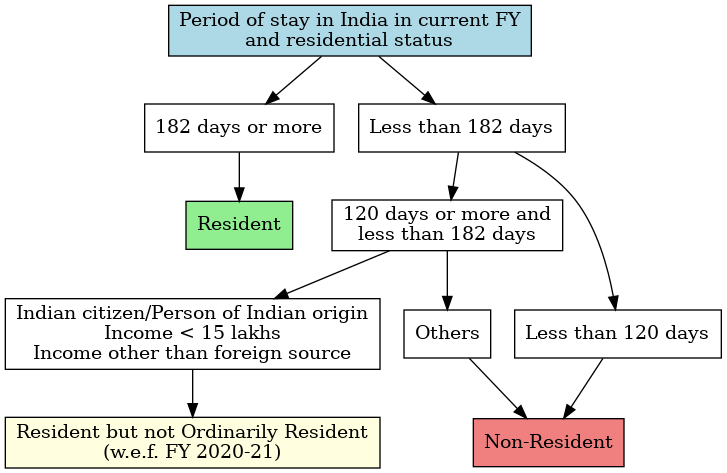

A taxpayer would qualify as a resident of India if he satisfies one of the following 2 conditions:

- Stay in India for a year is 182 days or more or

- Stay in India for the immediately 4 preceding years is 365 days or more and 60 days or more in the relevant financial year

Resident not ordinarily resident

If an individual qualifies as a resident, the next step is to determine if he/she is a Resident ordinarily resident (ROR) or an RNOR. He will be a ROR if he meets both of the following conditions:

- Has been a resident of India in at least 2 out of 10 years immediately previous years and

- Has stayed in India for at least 730 days in 7 immediately preceding years

Therefore, if any individual fails to satisfy even one of the above conditions, he would be an RNOR.

From FY 2020-21, a citizen of India or a person of Indian origin who leaves India for employment outside India during the year will be a resident and ordinarily resident if he stays in India for an aggregate period of 182 days or more.

However, this condition will apply only if his total income (other than foreign sources) exceeds Rs 15 lakh. Also, a citizen of India who is deemed to be a resident in India (w.e.f FY 2020-21) will be a resident and ordinarily resident in India.

NOTE: Income from foreign sources means income which accrues or arises outside India (except income derived from a business controlled in India or profession set up in India).

Non-Resident

An individual satisfying neither of the conditions of resident or nor resident not ordinary resident, as mentioned above would be a Non-Resident for the year.

Exceptions for determining residential status

There are following exceptions is there under which residential status will depends on various factors:

- An individual who is a citizen of India or person of Indian origin leaves India for employment during an FY, he will qualify as a resident of India only if he stays in India for 182 days or more. Such individuals are allowed a longer time greater than 60 days and less than 182 days to stay in India.

However, from the financial year 2020-21, the period is reduced to 120 days or more for such an individual whose total income (other than foreign sources) exceeds Rs 15 lakh.

- An individual who is a citizen of India who is not liable to tax in any other country will be deemed to be a resident in India. The condition for deemed residential status applies only if the total income (other than foreign sources) exceeds Rs 15 lakh and nil tax liability in other countries or territories by reason of his domicile or residence or any other criteria of similar nature.

The amendment can be further simplified as below-

Taxability in following different residential status

Resident: A resident will be charged to tax in India on his global income i.e. income earned in India as well as income earned outside India.

NR and RNOR: Their tax liability in India is restricted to the income they earn in India. They need not pay any tax in India on their foreign income. Also note that in a case of double taxation of income where the same income is getting taxed in India as well as abroad, one may resort to the Double Taxation Avoidance Agreement (DTAA) that India would have entered into with the other country in order to eliminate the possibility of paying taxes twice.

Determination of residential status of a company in India

Residential status of a company is determined as follows –

| Section | Company | Residential Status |

| 6(3)(i) | Indian Company | Always Resident in India (Notes 1) |

| 6(3)(ii) | A foreign company (whose turnover/gross receipt in the previous year is more than Rs. 50 crore) | It will be resident in India if its place of effective management (POEM), during the relevant previous year, is in India. (Notes 2) |

| 6(3)(iii) | A foreign company (whose turnover/gross receipt in the previous year is Rs. 50 crore or less) | Always non-resident in India (Notes 3) |

Notes:

- An Indian company is always resident in India. Even if an Indian company is controlled from a place located outside India (or even if shareholders of an Indian company controlling more than 51 per cent voting power are non-resident and/or located outside India), the Indian company is resident in India. An Indian company can never be non-resident.

- A foreign company is resident in India if its place of effective management (POEM), during the relevant previous year, is in India. For this purpose, the place of effective management means a place where key management and commercial decisions that are necessary for the conduct of the business of an entity as a whole are, in substance made.

- Provisions of section 6(3)(ii) shall not apply to a foreign company having turnover or gross receipts of Rs. 50 crore or less in a financial year. In other words, a foreign company (whose annual turnover/gross receipts is Rs. 50 crore or less) cannot be resident in India from the assessment year 2017-18 onwards.

Place of effective management (POEM)

“Place of effective management” (POEM) is an internationally recognized test for determination of residence of a company incorporated in a foreign jurisdiction. Any determination of the POEM will depend upon the facts and circumstances of a given case. The POEM concept is one of substance over form.

An entity may have more than one place of management, but it can have only one place of effective management at any point of time. Since “residence” is to be determined for each year, POEM will also be required to be determined on year to year basis. The process of determination of POEM would be primarily based on the fact as to whether or not the company is engaged in active business outside India.

Place of effective management in case company engaged in active business outside India

The place of effective management in case of a company engaged in active business outside India shall be presumed to be outside India if the majority meetings of the board of directors of the company are held outside India.

Active business outside India – A company shall be said to be engaged in “active business outside India” if –

- The passive income is not more than 50 per cent of its total income;

- Less than 50 per cent of its total assets are situated in India;

- Less than 50 per cent of total number of employees are situated in India or are resident in India; and

- The payroll expenses incurred on such employees is less than 50 per cent of its total payroll expenditure.

Passive income – “Passive income” of a company shall be aggregate of:

- Income from the transactions where both the purchase and sale of goods is from/to its associated enterprises; and

- Income by way of royalty, dividend, capital gains, interest or rental income;

However, any income by way of interest shall not be considered to be passive income in case of a company which is engaged in the business of banking or is a public financial institution, and its activities are regulated as such under the applicable laws of the country of incorporation.

Indian Income

Any of the following three is an Indian income —

- If income is received (or deemed to be received) in India during the previous year and at the same time it accrues (or arises or is deemed to accrue or arise) in India during the previous year.

- If income is received (or deemed to be received) in India during the previous year but it accrues (or arises) outside India during the previous year.

- If income is received outside India during the previous year but it accrues (or arises or is deemed to accrue or arise) in India during the previous year.

Foreign Income

If the following two conditions are satisfied, then such income is “foreign income” —

- Income is not received (or not deemed to be received) in India; and

- Income does not accrue or arise (or does not deemed to accrue or arise) in India.

The Incidence of Tax of “Indian Income” and “Foreign Income” is as Follows:

| Income and Resident Types | Resident in India | Non-Resident in India |

| Indian Income | Taxable in India | Taxable in India |

| Foreign Income | Taxable in India | Non Taxable in India |

Frequently Asked Questions (Residential Status in India)

Q. Can I be a Resident and RNOR at the same time?

No, you can only be one of the three: Resident, RNOR, or Non-Resident.

Q. Is foreign income taxable for RNORs?

No, RNORs are only taxed on their Indian income.

Q. What is POEM for foreign companies?

POEM is the place where key management decisions are made. If POEM is in India, the company is considered a Resident.

Q. How can I avoid double taxation?

You can claim relief under the DTAA if your income is taxed in India and another country.

Conclusion(Residential Status in India)

Determining your residential status is essential for accurate tax compliance. Whether you are a Resident, RNOR, or Non-Resident, understanding the rules can help you optimize your tax liabilities. For personalized advice, consult a qualified tax professional like Taxunplug for all your tax needs.

The information provided in above blog is for general informational only and should not be considered as legal or tax advice. Request you to please follow latest updated in reference to above details. We advise to consult with a qualified tax professional such as “Taxunplug” for all your tax needs.