Common Reasons Why Taxpayers Get GST Notices

Introduction

Receiving a GST notice can be stressful for any taxpayer. The Indian tax authorities issue these notices for various reasons, such as discrepancies in filings, non-compliance, or suspicious transactions. Understanding why taxpayers get GST notices can help businesses and individuals stay compliant and avoid penalties.

Most common reasons why taxpayers receive GST notices and how you can prevent them.

1. Mismatch in GST Returns

A significant reason for receiving a GST notice is mismatched data between different GST returns. Authorities’ cross-check details from GSTR-1 and GSTR-3B. If there are discrepancies, you may receive a notice for clarification or rectification.

How to Avoid It?

- Regularly reconcile your GST returns before filing.

- Verify sales and purchase details with suppliers.

- Use automated accounting software to reduce manual errors.

2. Discrepancies in annual return and reconciliation statement

Businesses require to file annual returns (GSTR-9) and reconciliation statements (GSTR-9C), wherever applicable, to summarize their financial activities for the year. However, discrepancies may arise between these and the periodic returns (GSTR-1 and GSTR-3B) filed throughout the year, potentially leading to notice.

How to Avoid It?

- Reconcile your monthly return with annual return

- Amend and correct the mismatch data in appropriate time.

- Opt for the GST compliance services from professionals like “Taxunplug” if required.

3. Late Filing or Non-Filing of Returns

GST returns must be filed on time as per the due dates. If you fail to file or delay your returns, the tax department may issue a notice, and you might have to pay penalties or interest.

How to Avoid It?

- Set reminders for GST return deadlines.

- Opt for the GST compliance services from professionals, like “Taxunplug” if required.

4. Excess Input Tax Credit (ITC) Claims

Claiming excessive ITC or claiming ITC without proper invoices can trigger GST notices. Tax authorities scrutinize ITC claims to prevent tax evasion. Section 16(2) of CGST Act, 2017 defines following pre-conditions for availing ITC:

- You are in possession of a tax invoice or debit note issued by a supplier registered under this Act, or such other tax paying documents as may be prescribed.

- You received the goods or services or

- subject to the provisions of section 41, the tax charged in respect of such supply has been actually paid to the Government, either in cash or through utilization of input tax credit admissible in respect of the said supply and

- He has furnished the return u/s 39 of CGST Act

- Payments to supplier (other than RCM ) will be made within 180 days from the date of issue of invoice, if failed, amount equal to ITC claim with interest will be added back to his outward tax liability.

How to Avoid It?

- Claim ITC only for eligible purchases.

- Validate all pre-conditions, which help in future compliances.

- Maintain valid tax invoices and records for ITC claims.

5. Turnover not matching with Income Tax Return

If your turnover shows a difference between the turnover reported in GST return and Turnover reported in Income tax return, authorities may send a GST notice for further investigation to identify any unreported income or sales.

How to Avoid It?

- Maintain proper sales records and justify any significant variations.

- Submit proper documentation if questioned by the tax department.

6. TDS/TCS Return discrepancies

TDS (Tax Deducted at Source) and TCS (Tax Collected at Source) under GST are crucial mechanisms to track and regulate tax compliance on specific transactions. Businesses liable to deduct or collect tax must file periodic TDS/TCS returns accurately. Any mismatch between the reported figures and actual transactions or failure to file returns can trigger GST notices.

How to Avoid It?

- Accurate Deduction & Collection.

- Reconciliation of Transactions.

- Timely Filing of Returns

7. E-Way Bill and Supply Mismatch

For inter-state transactions, E-Way bills are mandatory. If the details in E-Way bills don’t match the GST returns, it can lead to scrutiny and a GST notice.

How to Avoid It?

- Generate E-Way bills for all applicable transactions.

- Ensure the information in GST returns and E-Way bills is consistent.

8. Non-Compliance with GST Notices

If a taxpayer receives a GST notice and fails to respond within the given timeline, it can result in further legal actions, penalties, or even cancellation of GST registration.

How to Avoid It?

- Always check GST notifications and emails regularly.

- Respond to GST notices within the prescribed time frame.

9. Fake Invoicing and Tax Evasion

Issuing fake invoices or engaging in tax evasion is a serious offense. If tax authorities suspect fraudulent activities, they can issue a notice or initiate legal action.

How to Avoid It?

- Avoid engaging in fake invoicing practices.

- Ensure all transactions are genuine and backed by proper documentation.

10. Non-Reversal of ITC on Ineligible Transactions

If a taxpayer does not reverse the ITC for ineligible transactions, such as personal expenses or blocked credits, the tax department may issue a notice.

How to Avoid It?

- Identify and reverse ineligible ITC on time.

- Keep track of expenses and their eligibility under GST rules.

What to Do If You Receive a GST Notice?

If you receive a GST notice:

- Read the notice carefully – Understand the reason and the required action.

- Gather relevant documents – Collect invoices, returns, and other supporting records.

- Respond on time – Submit your response before the deadline.

- Seek professional help – Consult a tax expert like “Taxunplug” if needed.

List of notices which can be issued under GST

Following table highlight GST Notices as issued under the GST laws:

| S. No. | Name of Notice (Form) | Section of Law (CGST Act/ Rules) | Description | Action to be taken | Time limit to respond | What if, not responding of notices |

| 1 | REG-03 | Rule 9(2) | Clarification requiredon the information provided in the new registration application or amendment of GST registration | Reply, in form REG-04 with clarification, information and document, if any | Within 7 working days from the date of receiving the notice | Rejection of the application (inform the applicant electronically in form REG-05). |

| 2 | REG-17 | Rule 22(1) | SCNon why the GST registration not be cancelled | Reply, in form REG-18 with the reasons | Within 7 working days from the date of receiving the notice | Cancellation of GST registration (issuance of form REG-19) |

| 3 | REG-23 | Rule 23(3) | SCNon why the cancellation of GST registration must be revoked for the reasons laid down in the notice | Reply in form REG-24 | Within 7 working days from the date of receiving the notice | Cancellation of GST Registration will be revoked |

| 4 | REG-27 | Rule 24(3) | For cases relating to migration into GST from VAT regime, for not making application after obtaining provisional registration or not giving correct or complete details therein | Reply by applying in REG-26 and appear before the tax authority giving reasonable opportunity to be heard | None prescribed | Cancellation of provisional registration (in form REG-28) |

| 5 | GSTR-3A | Rule 68 | Default notice to non-filers of GST returns in GSTR-1 or GSTR-3B or GSTR-4 or GSTR-8 | File GST Returns along with late fees and interest, if any | 15 days from the date of receiving notice | Best judgement basis assessment by Dept. including penalty u/s 122 |

| 6 | CMP-05 | Rule 6(4) | SCN on eligibility to be a composition dealer | Necessary justification in form CMP-06 | 15 days of receipt of the notice | Penalty u/s 122 plus order (in form CMP-07) denying the benefit of the scheme |

| 7 | PCT-03 | Rule 83(4) | SCN for misconduct by the GST practitioner | Necessary justification | Within time prescribed in the SCN | Cancellation of the license as GST practitioner |

| 8 | RFD-08 | Rule 92(3) | SCN on rejection of GST refund made | Reply in form RFD-09 | Within 15 days of receipt of notice | Rejection order (in form RFD-06) |

| 9 | ASMT-02 | Rule 98(2) | Additional Information for provisional assessment under GST | Reply (in form ASMT-03 along with documents | Within 15 days of the service of the notice | Application may be rejected |

| 10 | ASMT-06 | Rule 98(5) | Additional information for final assessment under GST | Reply (in form ASMT-03 along with documents | Within 15 days of the service of the notice | Order, in form ASMT-07 may be passed ex-parte |

| 11 | ASMT-10 | Rule 99(1) | Notice for intimating discrepancies in the GST return after scrutiny | Reply in form ASMT-11 giving reasons for discrepancies | Within the time prescribed in the SCN or 30 days from the date of service of notice | Ex-parte assessment |

| 12 | ASMT-14 | Rule 100(2) | SCN – Assessment u/s 63 (best judgement assessment) | Appearance before the concerned authority | Within 15 days of the notice | Assessment order in form ASMT-15 |

| 13 | ADT-01 | Rule 101(2) | Notice for conducting Audit u/s 65 | Attend in person and/ or produce records | Within the time prescribed in the notice | Deemed that the taxpayer doesn’t possess necessary records and proceedings shall be initiated accordingly. |

| 14 | RVN-01 | Rule 109B | Notice u/s 108 issued by revisional authority | Reply within prescribed time and/ or appear before the authority | Within 7 working days of the serving of the notice | Ex-parte judgement |

| 15 | DRC-01 | Rule 100(2) & Rule 142(1)(a) | SCN for demand of tax (served along with DRC-02) | Reply, in form DRC-06. Payment in form DRC-03 | Within 30 days of the notice | Order passed with available details |

| 16 | DRC 10 | Rule 144(2) | Notice for Auction of Goods u/s 79(1)(b) | Pay outstanding demand as per form DRC-09 | As specified in the notice | Proceed with auction and sale |

| 17 | DRC-11 | Rule 144(5) & Rule 147(12) | Notice to the successful bidder | Pay the bid amount | Within 15 days from the date of auction | Re-auction |

| 18 | DRC-13 | Rule 145(1) | Notice to a third person u/s 79(1)(c) | Deposit the amount specified in the notice and reply in form DRC-14 | Not Applicable | Deemed to be a defaulter |

| 19 | DRC-16 | Rule 147(1) & Rule 151(1) | Notice for attachment and sale of immovable/movable goods/shares u/s 79 | Refrain from transferring/ creating charge on the assets | Not applicable | Prosecution and penalties |

How do I check if I have received a GST Notice

To check the notices issued by the Goods and Services Tax authorities, you need to follow the steps mentioned below:

- Go to the official GST portal and Login in your account

- You will be directed to the dashboard

- Click on the “User Services” under “services” tab from the left sided menu

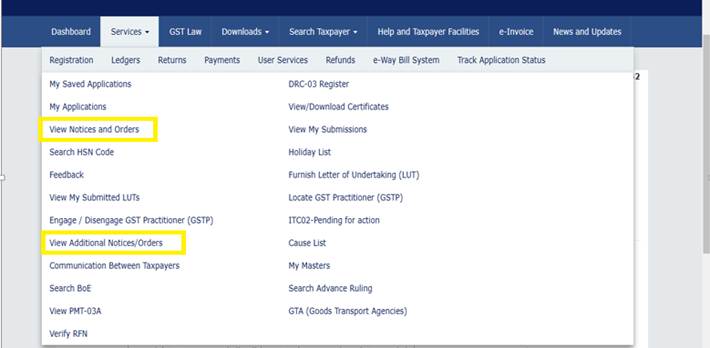

- Select the section “View notices and orders” or “View Additional Notices/Orders”

- A list of all notices and orders issued to you will appear. You can click on any notice to view its details.

Frequently Asked Questions (Common Reasons Why Taxpayers Get GST Notices)

Q1: What happens if I ignore a GST notice? Ignoring a GST notice can result in penalties, fines, or even cancellation of GST registration. It is best to respond promptly.

Q2: How do I check if I have received a GST notice? You can check your GST notices in the GST portal under the ‘Notices and Orders’ section or through email alerts from the tax department.

Q3: Can I get a GST notice even if I filed my returns on time? Yes, notices can be issued for mismatches, incorrect ITC claims, or any discrepancies in your filings.

Q4: How much time do I have to respond to a GST notice? The response time varies depending on the type of notice. Usually, the deadline is mentioned in the notice itself.

Q5: Can I challenge a GST notice? Yes, if you believe the notice is incorrect, you can challenge it by filing a reply with supporting documents.

Conclusion

Understanding the Common Reasons Why Taxpayers Get GST Notices can help businesses and individuals avoid unnecessary penalties. Regular compliance, accurate return filing, and prompt responses to notices are essential to staying safe from GST-related legal issues.

Common Reasons Why Taxpayers Get GST Notices

Facing an GST Notice? Connect with us by dropping your Name, Mobile and Email at Taxunplug. We will take care of all the sticky things and helps to take timely action, and ensure compliance to avoid legal complications.

The information provided in this blog is for general informational purposes only and should not be considered legal or tax advice. Please stay updated with the latest regulations related to the above details. We recommend consulting a qualified tax professional, such as Taxunplug, for expert assistance with all your tax matters.